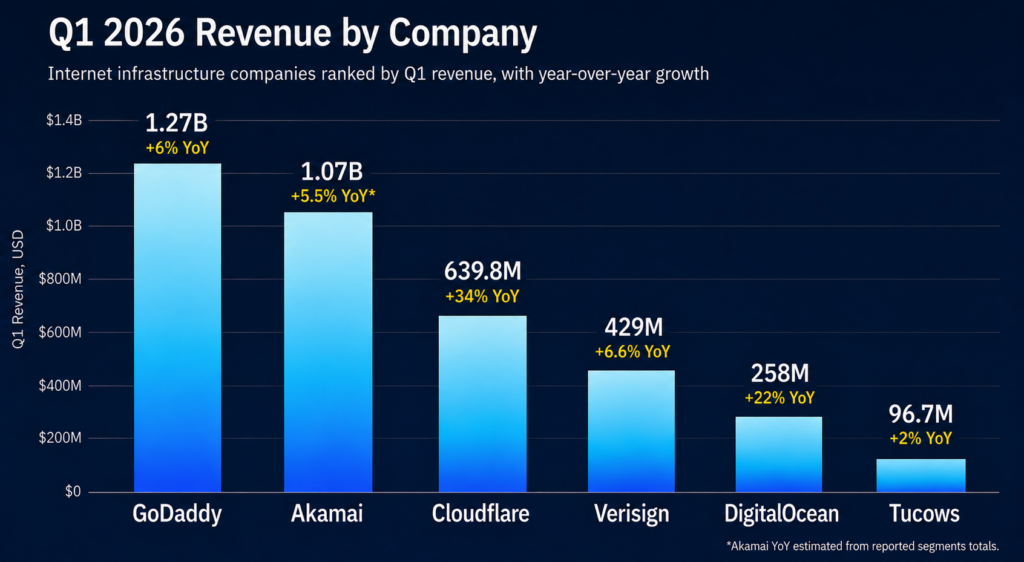

On the evening of May 7, 2026, two of the internet’s core infrastructure companies reported first-quarter earnings within hours of each other. Akamai announced a $1.8 billion, seven-year AI compute contract with an unnamed US frontier model provider, and its stock surged more than 26% in after-hours trading. Cloudflare reported $639.8 million in Q1 revenue, up 34% year-over-year, beat analyst expectations by roughly $18 million, raised full-year guidance, and saw its stock fall roughly 16% after disclosing it was cutting 1,100 employees, or 20% of its workforce, and posting Q2 guidance below analyst expectations. Both companies beat on revenue. The market’s verdict on each could not have been more different. The divergence is not about execution. It is about what kind of revenue the market is willing to pay for in 2026.

Akamai’s $1.8 Billion Deal: What a Seven-Year AI Compute Contract Actually Looks Like

Akamai’s Cloud Infrastructure Services segment grew 40% year-over-year to $95 million in Q1 2026. That is the fastest-growing part of the business, though still small relative to Security ($590 million, +11%) and the legacy Delivery segment ($389 million, -7%). The business that markets rewarded on May 7 was not the quarterly numbers. It was the signed commitment.

The $1.8 billion commitment, which CEO Tom Leighton described as the “largest customer deal in Akamai history,” comes from a leading US-based frontier model provider that Akamai has not named. The structure is a seven-year commitment for Cloud Infrastructure Services, meaning physical compute, not software or platform access. Revenue will not be material immediately: the company expects the deal to contribute $20 million to $25 million in Q4 2026 as the ramp begins. To support the contract, Akamai plans to spend $800 million to $825 million in capital expenditure over the next twelve months, with roughly $700 million deployed in the second half of 2026 and the remainder in early 2027.

This is not Akamai’s first AI compute deal of this kind. In February 2026, the company announced a separate $200 million commitment from another major US technology company described as at the forefront of the AI industry. The pattern is clear: Akamai is converting its existing distributed server footprint, originally built for content delivery, into GPU and compute infrastructure leased directly to AI labs at hyperscale contract terms. For a company whose traditional delivery business shrank 7% year-over-year in Q1, the pivot is working.

Cloudflare Beat the Quarter and Still Lost Nearly a Fifth of Its Market Cap

Cloudflare’s Q1 numbers were strong by most measures. Revenue of $639.8 million grew 34% year-over-year and beat consensus. The company raised its full-year 2026 revenue guidance to $2.805 billion to $2.813 billion and set Q2 guidance at $664 million to $665 million. Free cash flow was $84.1 million at a 13% margin. Non-GAAP EPS of $0.25 beat the $0.23 consensus.

The market sold the stock because of what came alongside those numbers: a plan to eliminate 1,100 positions globally, representing 20% of Cloudflare’s entire workforce. The company estimates restructuring charges of $140 million to $150 million, the majority of which will hit in Q2 2026. CEO Matthew Prince framed the cuts in AI terms: “AI is driving a fundamental re-platforming of the Internet and a paradigm shift in how software is created and consumed; it’s shaping up to be the biggest tailwind we’ve ever seen in Cloudflare’s history.” He also stated that AI use at Cloudflare grew 600% in the last three months, enabling smaller teams to handle work that previously required more headcount.

The layoff announcement was not the only catalyst for the sell-off. Cloudflare’s Q2 revenue guidance of $664 million to $665 million came in below analyst consensus of approximately $666 million. For a stock trading at a premium on growth expectations, even a small guidance miss amplifies the market’s reaction to any accompanying bad news. The combination of a guidance shortfall and a $140 million restructuring charge outweighed the Q1 revenue beat.

The market’s read was not that Cloudflare is in trouble. It was that the company is voluntarily absorbing a $140 million charge and significant operational disruption in pursuit of an AI platform bet whose payoff is future and uncertain. Akamai, by contrast, is receiving signed seven-year contracts with dollars attached. The market in May 2026 is pricing contracted infrastructure revenue at a premium over platform positioning, regardless of how compelling the platform story is.

Q1 2026 Across the Industry: GoDaddy, DigitalOcean, Verisign, and Tucows

The Akamai and Cloudflare results do not exist in isolation. Four other major companies reported Q1 2026 results over the preceding two weeks, and taken together they describe the same underlying split in sharper detail.

GoDaddy reported Q1 revenue of $1.27 billion, up 6% year-over-year, with free cash flow of $473.6 million, up 15%. The headline metric was average revenue per user growing 9% to $246 annually. GoDaddy added only 13,000 net new customers in the quarter on a base of 20.4 million, which is essentially flat, but it does not need subscriber growth when ARPU is compounding at 9%. The Airo AI Builder, launched in beta, reached an annualized bookings run rate of over $10 million within weeks. More significantly, customers acquired through Airo are attaching a second product 30% faster than non-Airo cohorts, which is the signal GoDaddy is watching: not raw AI revenue, but AI’s effect on monetisation depth per customer.

GoDaddy also announced a partnership with Cloudflare to give website owners control over how AI crawlers access their content, and introduced an Agent Name Service as an addressing system for AI agents. The product direction is clear: GoDaddy is positioning itself as infrastructure for the agentic web at the SMB layer.

DigitalOcean reported Q1 revenue of $258 million, up 22% year-over-year, with AI customer annual recurring revenue reaching $170 million, up 221% year-over-year. The company raised its full-year 2026 revenue guidance to $1.130 billion to $1.145 billion, representing 25-27% growth, and set its 2027 growth outlook above 50%. DigitalOcean’s model is the closest among public hosting companies to Akamai’s: it is selling GPU and compute infrastructure directly to AI developers, not a software layer on top of it. The difference is customer size. Akamai is landing frontier model labs at $1.8 billion. DigitalOcean is landing AI startups and developers at a fraction of that scale, but growing the segment at triple-digit rates.

Verisign reported Q1 revenue of $429 million, up 6.6% year-over-year, with the combined .com and .net domain base reaching a record 176.1 million names. The company also announced a .com wholesale price increase from $10.26 to $10.97, effective November 1, 2026, a 6.9% increase. Verisign does not compete in AI infrastructure. It controls the registry for the world’s most valuable top-level domain, raises prices at the rate its ICANN agreement permits, and earns consistent returns. It is not a growth story, but it is a structurally protected margin story that no amount of AI disruption is likely to reach in the near term.

Tucows reported Q1 revenue of $96.7 million, up 2%, with a net loss of $18.1 million and adjusted EBITDA of $11.7 million, down 15% year-over-year. The one bright spot was operating cash flow turning positive at $3.5 million, versus negative $11.3 million in Q1 2025. Tucows runs three businesses: a domain registrar (Tucows Domains), a platform for telecoms (Wavelo), and a fiber internet provider (Ting). None of them are AI infrastructure. The company is grinding toward cash flow breakeven while two of its three segments remain in investment mode. It is the clearest example in Q1 of what happens when a hosting-adjacent company has no AI story to sell.

What Is Working Across the Industry in 2026

Contracted AI compute is the highest-value product in the market. Akamai’s $1.8 billion win and DigitalOcean’s $170 million AI ARR are not the same type of deal, but they validate the same principle: physical infrastructure sold directly to AI workloads commands premium pricing and long contract terms. The companies closest to raw compute, at whatever customer tier, are seeing the fastest revenue growth and the strongest market reactions.

ARPU extraction from existing customers outperforms subscriber acquisition. GoDaddy’s 9% ARPU growth on a flat customer base, combined with Airo’s 30% faster second-product attach rate, confirms that AI-native tools embedded in the existing customer journey create measurable monetisation impact. Selling AI to 20 million existing customers is more efficient than acquiring 20 million new ones.

Security is growing everywhere it is offered. Akamai’s security segment grew 11% to $590 million in Q1. Cloudflare’s growth is driven partly by its security and network access products. Security is the one infrastructure category that AI is not threatening to commoditise; if anything, AI is expanding the threat surface and increasing demand for security tooling at scale.

What Is Not Working

Traditional content delivery is in structural decline. Akamai’s Delivery segment fell 7% year-over-year to $389 million. This is a category that built Akamai’s business over twenty years. The same pressure applies to any hosting provider whose primary value proposition is moving content fast: that margin is being competed away by hyperscaler CDNs and is not being replaced by AI-related demand.

Platform bets without hard contracts are being discounted. Cloudflare’s AI platform story (Workers AI, agentic infrastructure, AI crawl control) is strategically coherent. The market’s roughly 16% sell-off was not a rejection of the strategy. It was a valuation reset: in a market that just saw Akamai receive $1.8 billion in signed commitments, a platform narrative with optionality but no equivalent contracted revenue is worth less than it was six months ago. The restructuring charge amplified the discount.

Bulk subscriber growth without AI differentiation is losing ground. Companies that compete primarily on price for new subscribers, with no AI product to change the monetisation curve, face an increasingly difficult market. Tucows’ widening net loss alongside only 2% revenue growth illustrates the outcome.

The question that Q1 2026 does not answer is what happens when frontier model labs with $1.8 billion to spend on compute decide to build their own edge networks. Akamai’s contract is a seven-year commitment, which is a long time in an industry moving at this speed. For hosting providers watching the results from the sidelines, the immediate lesson is more actionable: the companies growing fastest in 2026 are the ones that have turned AI from a marketing position into a contracted revenue line.

Sources

- Akamai Reports First Quarter 2026 Financial Results, GlobeNewswire (official)

- Akamai Shares Surge 26% on $1.8B AI Infrastructure Deal, SiliconAngle

- Cloudflare Q1 2026 Financial Results, StockTitan (official 8-K)

- Cloudflare Stock Sinks 16% After Earnings, CNBC

- GoDaddy Q1 2026 Earnings Transcript, Yahoo Finance

- DigitalOcean Q1 2026 Financial Results, DigitalOcean Investor Relations (official)

- Verisign Q1 2026 Earnings Transcript, Yahoo Finance

- Tucows Q1 2026 Results, PR Newswire (official)

- Cloudflare and GoDaddy Partner to Help Enable an Open Agentic Web, Cloudflare (official)