Buried in this spring’s annual filings is a pattern that no hosting or web-presence company put in its press release, and it may be the most important commercial fact in the industry right now: the cost of acquiring a customer is inflating at the exact moment the machinery for acquiring them is breaking down. Across the public filers, marketing budgets hit record highs while customer counts stalled or fell, and one company after another quietly retired the volume metric it once led with. Each move is defensible in isolation. Together, and set against the demand-side data on what AI search is doing to the discovery funnel, they describe an industry giving up on volume growth and repricing the customers it already has. The specifics are in the box below; we went through the filings so the pattern is visible in one place.

The five companies, side by side (FY2025)

| Company | 2025 marketing spend (line item) | Spend as % of revenue | 2025 revenue (YoY) | Customers (YoY) |

|---|---|---|---|---|

| GoDaddy | $375.1M (marketing & advertising) | n/a | $4.95B (+8.3%) | 20.4M (down, 2nd year) |

| Wix | $514.3M (sales & marketing) | ~26% | $1.99B (+13.2%) | ~6.1M subs (down ~1%) |

| DigitalOcean | $82.4M (sales & marketing) | ~9% | $901.4M (+15.5%) | recast; volume de-emphasized |

| IONOS | €327.1M (selling) | 24.8% | €1,316.9M (+5.5%) | 6.63M (+307k) |

| Hostinger | not disclosed | n/a | €275.4M (+51%) | 4.6M (+35%) |

Figures from FY2025 filings (SEC EDGAR) and annual reports; dollar and euro amounts are not currency-adjusted. GoDaddy reports a narrower “marketing and advertising” line, so its spend-to-revenue ratio is omitted for comparability.

- The demand backdrop: Pew found users click a search result on just 8 percent of Google visits with an AI summary versus 15 percent without; GoDaddy’s own 10-K now lists AI tools as a risk to demand for its products.

- The historical anchor: GoDaddy’s 2017 cohort disclosure shows it once acquired ~5.0M gross customers on $253.2M of marketing, roughly $51 per gross add; that arithmetic no longer appears in the current filings.

GoDaddy: The Extraction Model, Fully Ripened

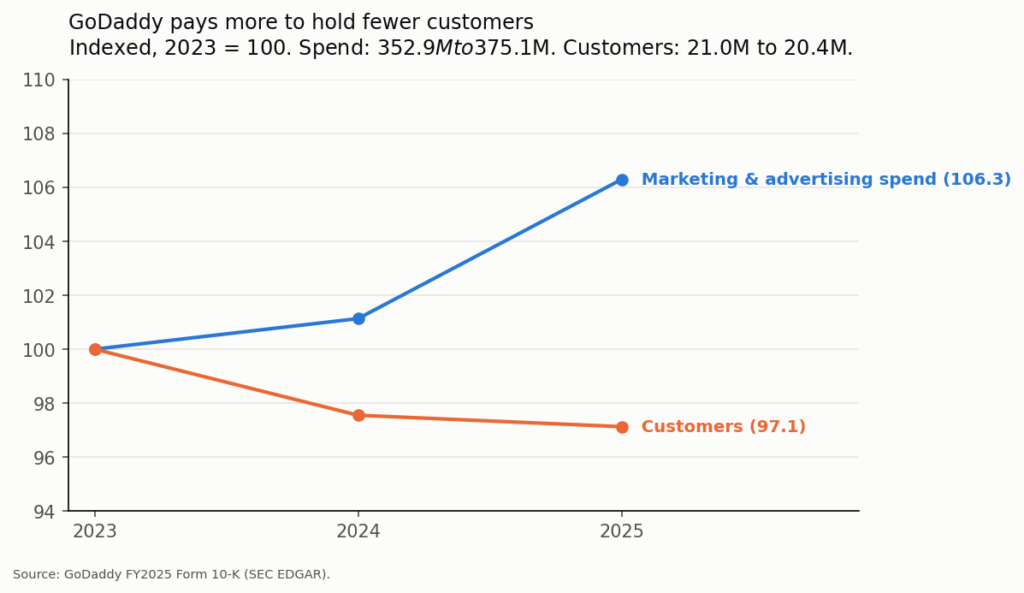

GoDaddy’s FY2025 10-K is the cleanest specimen because the company discloses the full triangle: spend, customers, and ARPU. Marketing and advertising expense rose 5.1 percent in 2025 to $375.1 million, which the filing attributes to “an increase in discretionary advertising spend in support of our strategic initiatives, including building broader awareness of our GoDaddy Airo experience.” Customers ended 2025 at 20.42 million, down from 20.51 million in 2024 and 21.03 million in 2023: two consecutive years of net customer decline at the industry’s largest player. What grew instead is the invoice. ARPU climbed from $203 in 2023 to $220 in 2024 to $242 in 2025, up 19 percent in two years, and reached $246 by Q1 2026. Revenue rose 8.3 percent to $4.95 billion.

The model works, and this publication has documented its components all year: renewal-price spreads, attach-rate pushes, AI upsells. But note what the spend is now buying. In its 2017 cohort disclosure, GoDaddy acquired roughly five million gross customers with $253.2 million of marketing, about $51 per gross addition. In 2025 it spent half as much again in absolute terms and the customer count fell. Marketing at GoDaddy no longer purchases growth; it purchases the slowing of decline, which is a materially different return on the same line item. The Q1 2026 filing adds a telling coda: GoDaddy cut marketing 7.8 percent year on year, and the customer base stayed flat anyway. Management appears to have run the experiment and reached the same conclusion.

The industry leader’s acquisition arithmetic, indexed. Source: GoDaddy FY2025 Form 10-K.

Wix: $514 Million, Minus 1 Percent, Then Silence

Wix’s 20-F shows the same shape with less cushion. Sales and marketing expense jumped from $425.5 million to $514.3 million in 2025, growing about 1.6 times as fast as revenue (13.2 percent, to $1.99 billion). Premium subscriptions, the metric Wix built its equity story on, fell about one percent to roughly 6.1 million. The filing’s explanation is candid: “Our strategic focus on higher-value users resulted in fewer gross subscription additions,” followed by the operative sentence, “we will no longer provide our total number of premium subscriptions on a regular basis.” A company does not retire a headline KPI that is about to improve. Registered users still grew, from 282.4 million to 304.2 million, but registered users are unmonetized top-of-funnel, and the year’s figures include the acquired Base44 business. The honest reading is that Wix now pays more than half a billion dollars a year to run in place on paying customers, and has chosen, rationally, to redirect the market’s attention toward revenue per subscription rather than subscriptions. That is the same pivot as GoDaddy’s, executed with less ARPU headroom and a bigger marketing bill.

DigitalOcean, IONOS, and Hostinger: Three Other Ways This Goes

DigitalOcean is the counterexample that proves the funnel problem is channel-specific. Its sales and marketing spend was $82.4 million in 2025, held at “approximately 9 percent of our revenue” for the third straight year, about a third of Wix’s ratio, while revenue grew 15.5 percent to $901.4 million. Self-serve, product-led acquisition aimed at developers still works at reasonable cost, because developers do not arrive through the Google-search shopping funnel that AI Overviews is dismantling. But even DigitalOcean quietly reworked its customer metrics, shifting the emphasis to higher-value customers and recasting prior periods, because it does not consider the low-spend cohort “a good predictor of our future growth.” Even the volume outlier no longer wants to be measured on volume.

IONOS, in its first years as a separately listed company, publishes the most honest European numbers. Selling expenses were €327.1 million in 2025, 24.8 percent of revenue, of which purchased marketing and advertising services rose 13 percent to €125.3 million. Paying customers grew by 307,000 to 6.63 million. Dividing the selling line by the net additions is crude, since most of that spend defends the existing base, but the crudeness is the point when the same ratio is applied to everyone: roughly €1,065 of selling spend per net added customer, for customers whose entry-level products bill tens of euros a year. The unit economics only close because retention is long and upsell is systematic, which is precisely why the whole industry is converging on the same two levers.

And then there is Hostinger, the private outlier, which reported €275.4 million of 2025 revenue, up 51 percent, and 4.6 million clients, up 35 percent, without disclosing marketing spend; its stated cost story is on the other side of the ledger, with its Kodee AI handling 81 percent of support interactions. Growth by volume still exists in hosting. It is just no longer being achieved by the companies that file with the SEC.

Why the Funnel Is Repricing: The Demand Side

The spend inflation has a cause, and it is measurable. Pew Research’s study of 68,879 real Google searches found that when an AI summary appears, users click a traditional result on 8 percent of visits, versus 15 percent without one, and click a source inside the summary just 1 percent of the time. The paid and organic search funnel that built every web-presence brand of the 2010s now converts roughly half as well at the top, which mechanically raises the price of every acquired customer downstream. The affiliate-review layer that supplemented it is weakening alongside, as we documented in our affiliate-channel analysis. GoDaddy itself now says it in the risk factors of its 10-K: the evolution of AI-powered tools “could negatively impact the demand for certain of our products and services, including domain names, aftermarket…” When the largest customer-acquirer in the industry files that sentence with the SEC while cutting its marketing budget and holding retention at 85 percent, the strategy is legible: stop bidding for scarcer new demand and monetize the installed base.

What the C-Level Should Take From the Filings

Three readings, in rising order of consequence.

- Benchmark yourself against the right ratio. The spread between DigitalOcean’s 9 percent of revenue and Wix’s 26 percent is the difference between product-led and funnel-led acquisition economics. Any host still buying customers through search and affiliates should assume its true CAC has inflated materially since 2023 even if the invoice from the ad platforms looks stable, because the funnel behind those invoices converts at the Pew numbers now.

- Read metric retirements as strategy disclosures. Wix hiding subscriptions, DigitalOcean recasting its metrics, GoDaddy leading every release with ARPU: these are companies telling you, in accounting language, that the volume era of web presence is over for them. For a smaller host, that is not bad news; it means the giants’ marketing machines are being pointed at wallet share, not at land grab, and price-sensitive volume segments are being conceded. Hostinger’s 35 percent client growth shows who is collecting them.

- The extraction model has a horizon. ARPU-led growth on a shrinking base works while retention holds near 85 percent, and every renewal-price and attach-rate lever the industry pulls, which this publication tracks in its renewal-multiplier work, tests that retention. The filings we will read next spring will show whether 2026 was the year the base noticed.

The customer count lines to watch are already public; from this year on, we will keep reading them so you do not have to.

Methodology

All company figures were taken directly from primary filings and verified on SEC EDGAR or the companies’ investor-relations publications on July 3, 2026: GoDaddy’s FY2025 Form 10-K (filed February 25, 2026; marketing and advertising expense, customer counts, ARPU, retention, the 2017 cohort disclosure, and the AI risk-factor language) and Q1 2026 Form 10-Q; Wix’s FY2025 Form 20-F (filed March 5, 2026; expense lines, registered users, premium subscriptions and the disclosure-discontinuation statement, with the Base44 consolidation noted); DigitalOcean’s FY2025 Form 10-K (filed February 24, 2026; expense ratio, revenue, the customer-metric redefinition and new counts); the United Internet AG and IONOS Group SE 2025 annual reports (selling expenses, marketing services line, customer additions). Hostinger figures are from its published 2025 results (private company, unaudited disclosure). Squarespace, now private under Permira, is excluded from current-year comparisons; its last full-year public figures (FY2023: sales and marketing at 34.5 percent of revenue) inform the historical context. The €1,065-per-net-add and $51-per-gross-add ratios are our arithmetic on the cited disclosed figures, and their limitations (selling spend also defends the existing base; gross versus net additions differ) are stated where used. Demand-side figures are from Pew Research Center’s July 2025 click-through study. We found no primary-source confirmation of specific 2025–2026 hosting-affiliate commission cuts and therefore assert none.

Sources

- GoDaddy FY2025 Form 10-K - SEC EDGAR

- GoDaddy Q1 2026 Form 10-Q - SEC EDGAR

- Wix.com FY2025 Form 20-F - SEC EDGAR

- DigitalOcean FY2025 Form 10-K - SEC EDGAR

- United Internet AG Annual Report 2025 (Business Applications segment)

- IONOS Group SE Annual Report 2025 (selling expenses, customer additions)

- Hostinger 2025 financial results - Hostinger

- Google users are less likely to click on links when an AI summary appears - Pew Research Center

- Squarespace FY2023 Form 10-K (final public-company filing) - SEC EDGAR