When a hosting renewal arrives at three or five times the signup price, the industry’s explanation is costs: hardware, energy, support, inflation. This publication has measured the pricing side of that story in detail, and the Renewal Multiplier Index we published on June 11, 2026 found multipliers running from 1.0x to 5.3x with no cost story that could explain the spread. The better explanation sits on the other side of the ledger, and it is the one nobody puts in the renewal email. The hosting industry is, to a degree its customers rarely see, a portfolio of leveraged private-equity positions, and the most heavily indebted operator in the business went through a debt restructuring in December 2025 that rating agencies treated as comparable to a distressed exchange. Who owns your host, what they paid, what they borrowed to pay it, and when that debt comes due will do more to shape your invoice, your product roadmap, and your host’s survival odds through 2028 than any technology decision the company makes. So we mapped it: every major operator’s ownership and debt against our own pricing measurements. The result reads less like an industry and more like four different businesses wearing the same logo wall.

Key facts, compiled June 12, 2026 (sources: SEC and registry filings, rating-agency actions, company statements; full list below)

- Newfold Digital (Bluehost, HostGator, Network Solutions; Clearlake + Siris) carries roughly $3.5B of debt at about six times earnings per Bloomberg; Moody’s cut it from B3 at the 2021 buyout to Caa1 (February 2025) and Caa3 (September 2025); on December 9, 2025 it closed terms on $100M of new money priced around 5.75 points over benchmark, with maturities extended and parts of the debt discounted

- The same company’s renewal prices are the ones machines cannot read: our Renewal Multiplier Index found Bluehost and HostGator serving renewal prices as a literal “$x.xx” template to automated readers, while debt-free SiteGround publishes its 5.3x in the open

- The tooling layer is being used as a dividend source: Bloomberg reported in October 2025 that CVC was in talks for a ~$1B private-credit loan on WebPros (cPanel, Plesk, WHMCS) to refinance a $540M loan and fund a dividend recapitalization; the Wall Street Journal reported in September 2025 that CVC was also nearing a majority stake in Namecheap at ~$1.5B

- The sponsor roll call: Permira holds Squarespace ($7.2B take-private, October 2024, financed with a $2.65B private-credit loan from Blackstone, Blue Owl, and Ares); Hg and CPP Investments hold team.blue (€4.8B valuation, July 2024); Cinven and Ontario Teachers’ hold group.one; KKR holds Contabo; Oakley Capital backs hosting.com; One Equity Partners holds Liquid Web

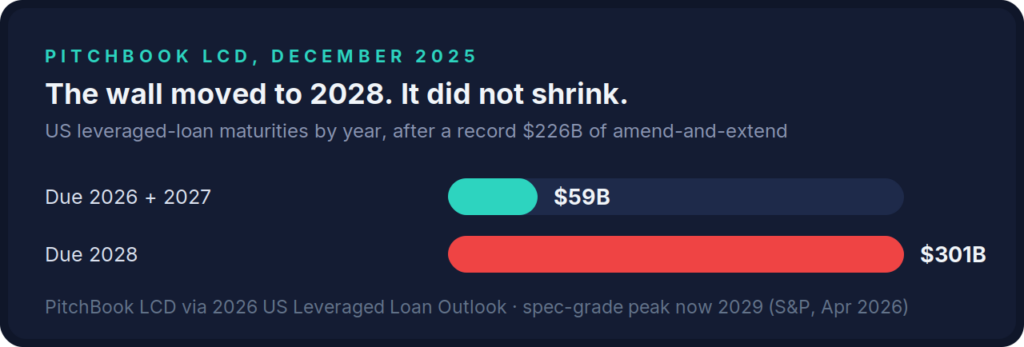

- The maturity wall moved rather than shrank: after a record $226B of amend-and-extend in 2024, US leveraged-loan maturities due 2026–2027 fell to $59B while 2028 ballooned to $301B (PitchBook LCD), and S&P says speculative-grade maturities now peak in 2029; distressed restructurings were roughly 65% of 2025 corporate defaults (Moody’s)

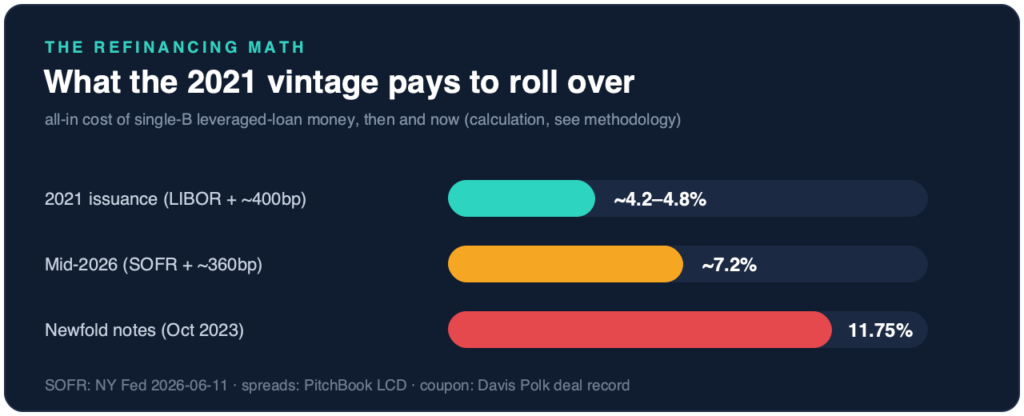

- The 2021 vintage refinances ~270–300bp higher: single-B loan money cost ~4.2–4.8% all-in in 2021 against ~7.2% in mid-2026 (SOFR 3.60% plus LCD spreads), and the ECB raised rates for the first time since 2023

- The counter-cohort is public or founder-owned: GoDaddy runs 1.6x net leverage and returned its entire $1.6B 2025 free cash flow as buybacks; IONOS runs 1.4x with record margins; DigitalOcean cleared its $1.5B zero-coupon convertible wall in August 2025; SiteGround, InterServer, and Hostinger carry no reported buyout debt at all

Same Invoice, Four Balance Sheets

Take the renewal multiplier table we published and ask one new question of every row: where does the renewal premium go? The answers sort the industry into four species. At SiteGround, founder-owned since 2004 with no private-equity involvement on record and a net margin north of 50% in its last press-reported registry filings, the 5.3x multiplier is profit, accruing to the people who built the company. At IONOS, listed in Frankfurt at a conservative 1.4x net debt to EBITDA, the 1.7–2.0x multipliers fund record margins and dividends to public shareholders, United Internet first among them. At GoDaddy, public and measured, the machine is explicit: $1.6B of 2025 free cash flow, $1.6B of 2025 share repurchases, and a Q1 2026 print of 13,000 net customer additions against 9% ARPU growth, extraction as a shareholder-returns program, run from a balance sheet (1.6x net leverage) that could absorb a recession. And at Newfold Digital, the owner of Bluehost and HostGator, the renewal premium services approximately $3.5 billion of debt at roughly six times earnings, a stack assembled through the 2021 take-private of Endurance International ($3.0B including debt) and its merger with Web.com under Clearlake Capital and Siris Capital.

Our own pricing data adds the detail that ties the species together. The Renewal Multiplier Index could not measure Bluehost or HostGator, because both serve renewal prices to automated readers as an unrendered “$x.xx” template, and GoDaddy and Namecheap block retrieval outright. The transparency gradient runs exactly along the balance-sheet gradient: the operators with the least to explain publish their multipliers in the open, and the operators whose renewal premium has a lien on it are the ones a machine cannot price. We do not claim intent; we claim the correlation, and it is complete across our sample.

The Leveraged Cohort: A Map of Who Holds What

The sponsor map, assembled from deal announcements and filings, looks like this:

- Clearlake and Siris hold Newfold.

- Permira holds Squarespace after the $7.2B take-private completed in October 2024, financed with a $2.65B private-credit loan led by Blackstone with Blue Owl and Ares, one of the largest direct-lending packages ever written for a web platform.

- Hg and CPP Investments hold team.blue, the 60-brand European roll-up valued at €4.8B in July 2024, when Canada’s national pension plan paid roughly €550M for about 20%.

- Cinven and Ontario Teachers’ hold group.one plus dogado, a 2022 transaction in which Cinven’s Fund 6 sold the asset to Cinven’s Fund 7, the sponsor selling to itself with a pension co-investor, financed in part by CVC’s credit arm.

- KKR took the majority of Contabo in 2022, handing Oakley Capital a greater-than-10x return on a 2019 investment.

- Oakley recycled those proceeds into its World Host Group roll-up, now branded hosting.com, which bolted on A2 Hosting in January 2025.

- One Equity Partners has held Liquid Web through its CloudOne Digital holding company since 2023.

- Silver Lake has sat on its 2018 $250M position in WP Engine for eight years, through a legal war with Automattic that has now outlived two trial calendars.

Three structural facts in that map matter more than any single deal.

First, almost none of these positions is young: Silver Lake is eight years in, Clearlake five, Cinven seven on the original group.one purchase. Private equity underwrites five-year holds; an aging position with no exit produces continuation funds, dividend recaps, and price increases, all three of which this industry now exhibits.

Second, the assets circulate among sponsors rather than exiting: fund-to-fund sales, sponsor-to-sponsor trades, minority pension stakes. The consolidation map we published counted the H1 2026 deals; the capital map explains them, because 30,000 unsold portfolio companies industry-wide (Bain’s count) need liquidity events and hosting’s recurring revenue still prices at 9x EBITDA or better.

Third, the renewal invoice is the debt service: a leveraged roll-up’s revenue lever is the installed base’s renewal rate, which is why the renewal-jump regulation story we have tracked since May 2026 (New York’s GBL §527-a, effective November 2025) is, underneath, a story about whose capital structure can tolerate notice requirements.

Newfold Is the Exhibit, Not the Exception

This publication has covered Newfold’s operating trouble separately: over a million subscribers lost between 2023 and early 2026, roughly 17% of the base, and the steepest .com transfer losses among major registrars. Here it serves as the cohort’s controlled experiment, because its capital structure is the only one in the private cohort that rating agencies narrate in public. The 2021 buyout was financed at B3 with a $1.935B term loan plus a $465M delayed draw and a revolver. By October 2023, with rates at their peak, Newfold had to price $515M of secured notes at 11.75%, a coupon that tells you what the market already thought. In February 2025 Moody’s cut to Caa1, citing refinancing risk on a $380M revolver due February 2026 with $223M drawn; S&P went to CCC+ the same week. In September 2025 Moody’s cut again, to Caa3, “as debt maturity approaches.” Through the autumn, per Bloomberg, Clearlake negotiated side pacts with creditors including PIMCO, GoldenTree, and Blackstone, and on December 9, 2025 the company announced the deal: $100M of new financing at roughly 5.75 points over benchmark, maturities pushed to 2029, parts of the stack discounted, tighter covenants. S&P cycled a downgrade and then a January 26, 2026 upgrade around the transaction, the standard sequence around exchanges the agencies treat as distressed. Along the way, Newfold bought MarkMonitor for $302.5M in 2022 and sold it three years later in a transaction it framed as focusing on core brands: buying at the top of the cycle, selling to raise liquidity at the bottom of its rating.

The C-level reading is not “Newfold is in trouble”; our previous piece covered that. It is that every mechanism in the Newfold sequence is general: the 2021-vintage debt, the rate shock on refinancing, the amend-and-extend, the asset sale, the new money from private credit at a premium, the renewal-price dependence throughout. The rest of the leveraged cohort is unrated and private, which means there is no Moody’s narration when the same mechanics operate behind team.blue’s serial acquisitions or group.one’s fund-to-fund sale. The absence of a public rating is not the absence of the math.

Amend-and-extend cleared the near years and stacked the wall in 2028; S&P now puts the speculative-grade peak in 2029. Data: PitchBook LCD, December 2025; S&P Global Ratings, April 2026.

The Toll Booth Pays the Sponsor First

One layer of the map deserves its own section, because it touches every host that is not a hyperscaler. WebPros, owner of cPanel, Plesk, and WHMCS, the control-panel and billing tooling under tens of millions of websites, has been owned by CVC since December 2019, when Oakley exited at 6.7x its money. In October 2025, Bloomberg reported CVC in talks with private-credit funds for a roughly $1B unitranche at around 525bp over SOFR, to refinance a $540M loan and fund a dividend recapitalization, a transaction that, as reported, pays the sponsor by borrowing against the toll booth’s future fees. We could not confirm the loan’s closing and report it as reported. In the same window, the Wall Street Journal reported CVC nearing a majority stake in Namecheap at roughly $1.5B including debt, a deal that has never been confirmed by either party and which we likewise carry strictly as reported. If both reported positions are real, one sponsor sits on the industry’s tooling monopoly and one of its two largest retail storefronts simultaneously, with the tooling layer’s pricing schedule (the cPanel licensing rounds this publication has tracked for two years, the next due in September 2026) as the natural instrument for servicing the borrowing. For every reseller and white-label host downstream, that is a cost line set by someone else’s dividend math.

The Wall Moved to 2028, Which Is Worse News Than It Sounds

The reassuring read of the credit data is that the wall receded: US leveraged-loan maturities due 2026–2027 collapsed from $195B to $59B during 2025 as borrowers refinanced and extended. The accurate read is that it moved: $301B now matures in 2028, S&P’s April 2026 research puts the global speculative-grade peak in 2029, and the extensions were bought with exactly the tools the hosting cohort has been using, a record $226B of amend-and-extend in 2024, payment-in-kind features near multi-year highs, and distressed restructurings running at roughly 65% of all corporate defaults in 2025 per Moody’s. The loan default rate itself ran near 7.5–7.9% around the turn of the year, double its historical average and concentrated, Moody’s notes, precisely in smaller, floating-rate, PE-owned borrowers, the demographic profile of a hosting roll-up. And the rate relief the extensions were betting on has stalled: the Fed has held at 3.50–3.75% since December 2025, and on June 11, 2026, the ECB raised rates for the first time since 2023. The arithmetic for the 2021 vintage is unforgiving: money borrowed at ~4.2–4.8% all-in rolls today at ~7.2%, with the entire gap in the base rate. For hosting customers the translation is simple: the extraction era does not wind down, it has a 2028–2029 deadline, and every quarter of high rates between now and then is a quarter in which the renewal lever, the licensing lever, and the asset-sale lever are the only ones that move a leveraged owner’s numbers.

What the 2021 vintage pays to roll over, with Newfold’s 2023 coupon marking what stressed issuance into the rate peak cost. Calculation from NY Fed SOFR and PitchBook LCD spreads; methodology below.

The Counter-Cohort, and an Honest Complication

The map has a second half, and it is where the share is going. DigitalOcean provides the clean textbook case: it faced the sector’s single largest maturity, $1.5B of zero-coupon convertibles due December 2026, and simply dealt with it in August 2025, issuing $625M of new converts due 2030 and a $380M term loan and repurchasing $1.19B of the old notes below par, no drama, because a listed company with real free cash flow can. IONOS grew 5.5% in FY2025 at a record 36.8% EBITDA margin and 1.4x net leverage, having repaid its shareholder loan, with Warburg Pincus fully exited in March 2025 in an orderly, staged selldown: private-equity entry and exit as the system is supposed to work. OVHcloud sits at 2.7x after a capex-heavy year, with the Klaba family above 80% after a €350M buyback, listed but family-governed. And Hostinger, the operator our Newfold coverage identified as the largest single taker of the leveraged cohort’s customers, grew revenue 51% in 2025 to €275M, its fourth consecutive year above 50%, on a balance sheet with no reported buyout debt and a founder-led register (a roughly 31% minority sold in 2021 to a vehicle of German hosting veterans Jochen Berger and Thomas Strohe, the co-founders of Host Europe Group, is the closest thing to outside capital in the structure).

The honest complication, and the reason this article is not a morality play about debt: the highest multiplier in our index belongs to a debt-free company. SiteGround’s 5.3x funds founder margins, not coupon payments, and InterServer proves at 1.0x that a founder-owned host can also simply not do this. Pricing power in hosting comes from switching costs and inattention, and it exists at every capital structure. What the balance sheet determines is not whether the lever exists but what happens when it stops working. A founder who over-prices loses share and adjusts; a public company that over-prices misses guidance and adjusts; a leveraged sponsor that over-prices and still cannot cover the stack does what Newfold did in December, and the customers inherit the consequences of the workout: sold assets, frozen roadmaps, support cuts, and brands that change hands in transactions optimized for creditors. The species matters at the boundary, and 2028 is the boundary.

What a Buyer, and a Board, Does With This

For a company that buys hosting, this map converts into four due-diligence questions that almost nobody asks at procurement:

- Who owns the operator, and what fund vintage is the position? A 2021-vintage sponsor position in year five behaves differently from a public company or a founder.

- When does their debt mature? For the rated names this is public; for the unrated, the proxy is behavior: dividend recaps, asset sales, and sudden licensing repricings are the observable surface of a maturity approaching.

- Is the renewal price machine-readable? Our index suggests opacity is not random; treat an unreadable renewal price as a data point about the seller, and contract accordingly, with renewal caps written in, which New York’s §527-a notice regime now makes easier to demand.

- What is the exit path if the operator restructures? The time to test your backup and migration plan, per our backup-economics analysis, is before the workout, not during.

For operators, the same map is the targeting document the counter-cohort is already using: every leveraged competitor’s installed base is, between now and 2028, a customer-acquisition pool priced by someone else’s interest schedule. Hostinger’s 51% growth did not come from nowhere; it came, in meaningful part, from the cohort this article maps. And for the sponsors themselves, the lesson of the year is that the industry’s two most credible operators of scale, GoDaddy and IONOS, are the ones whose owners chose markets over leverage. The renewal invoice is the same piece of paper either way. What stands behind it is not.

How We Verified This

Ownership, deal, and debt facts come from the SEC filings, company and sponsor press releases, rating-agency actions, issuer annual reports, and financial press listed below. Two items are reported but unconfirmed, and carried strictly with attribution: the WebPros dividend recapitalization (Bloomberg, October 2025) and the CVC/Namecheap stake (WSJ, September 2025). The exact S&P rating letters around Newfold’s December 2025 exchange sit behind access controls, so we describe the sequence without asserting them. Companies named as debt-free or low-debt (SiteGround, InterServer, Hostinger) are described from the absence of any reported leveraged transaction, not from a verified balance sheet. The 2021-versus-2026 loan-cost comparison is our own calculation from NY Fed SOFR (3.60%, June 11, 2026) and PitchBook LCD spreads; the renewal multipliers are our own measurement.

Sources

- Endurance International to be acquired by Clearlake Capital, ~$3.0B (November 2, 2020) - GlobeNewswire (official)

- Endurance 8-K: February 10, 2021 credit agreement ($1,935M term loan, $465M delayed draw) - SEC EDGAR

- Newfold Digital $515M 11.750% senior secured notes due 2028 (October 2023) - Davis Polk deal record

- Moody's downgrades Newfold to Caa1 on refinancing risk (February 14, 2025) - Moody's via Investing.com

- Clearlake's Newfold Seeks Support for Debt Deal Via Side Pacts (October 17, 2025) - Bloomberg

- Newfold Digital secures $100 million investment (December 9, 2025) - Newfold (official); terms per Bloomberg (December 9, 2025)

- Clearlake's Newfold finalizes terms for $100M financing (deal terms) - Bloomberg (December 9, 2025)

- Permira completes acquisition of Squarespace (October 17, 2024) - Permira (official)

- $2.65B private-credit financing for Squarespace - Bloomberg (May 13, 2024)

- CPP Investments takes ~20% of team.blue at €4.8B (July 10, 2024) - CPP Investments (official)

- Cinven and Ontario Teachers' combine group.ONE and dogado (December 2022) - Cinven (official)

- Oakley agrees sale of Contabo to KKR at >10x gross return (2022) - Oakley Capital (official)

- Oakley sells WebPros to CVC Fund VII (December 2019) - Oakley Capital (official)

- CVC in talks for ~$1B WebPros loan including dividend recap (October 7, 2025) - Bloomberg

- WSJ-reported CVC majority stake in Namecheap at ~$1.5B (September 12, 2025) - Domain Name Wire citing the Wall Street Journal

- One Equity Partners acquires Liquid Web, forms CloudOne Digital (2023) - One Equity (official)

- WP Engine: $250M from Silver Lake (January 4, 2018) - WP Engine (official)

- GoDaddy Q4/FY2025 results: $5.0B revenue, $1.6B FCF, $3.8B debt, 1.6x net leverage, $1.6B buybacks - SEC EDGAR (official)

- DigitalOcean closes $625M converts due 2030, repurchases $1,187.7M of 2026 notes (August 18, 2025) - Business Wire (official)

- IONOS Annual Report 2025: €1.317B revenue, 1.4x net debt/adjusted EBITDA - IONOS Group (official)

- OVHcloud FY25 results: €1,084.6M revenue, 2.7x leverage (October 21, 2025) - OVHcloud (official)

- Hostinger 2025 financial results: €275.4M revenue, +51% (February 23, 2026) - Hostinger (official)

- 2026 US Leveraged Loan Outlook: 2026–27 maturities $59B, 2028 $301B - PitchBook LCD (December 2025)

- Record $226B amend-and-extend in 2024 - PitchBook LCD

- Global Refinancing: Speculative-Grade Maturities Now Peak in 2029 (April 27, 2026) - S&P Global Ratings

- US corporate default risk in 2026: loan defaults ~7.5–7.9%, distressed restructurings ~65% of corporate defaults - Moody's

- ECB raises key rates 25bp, first hike since 2023 (June 11, 2026) - European Central Bank (official)

- SOFR 3.60% (June 11, 2026) - New York Fed (official)