A new intelligence report from ShareShift.io, a web market analytics firm, analyzed over three million new active domains registered across European ccTLDs and the .ai zone in Q2 2026. The headline finding: roughly 95% of new sites on traditional European hosting infrastructure have no embedded AI features. Meanwhile, fully integrated platforms like Wix are shipping AI-enabled sites by default, and Vercel is quietly capturing high-value developers before traditional hosts get a first pitch. The data points to a structural divide that price cuts and server upgrades will not close.

Vercel Is Winning New Developers Before Traditional Hosts Can Pitch Them

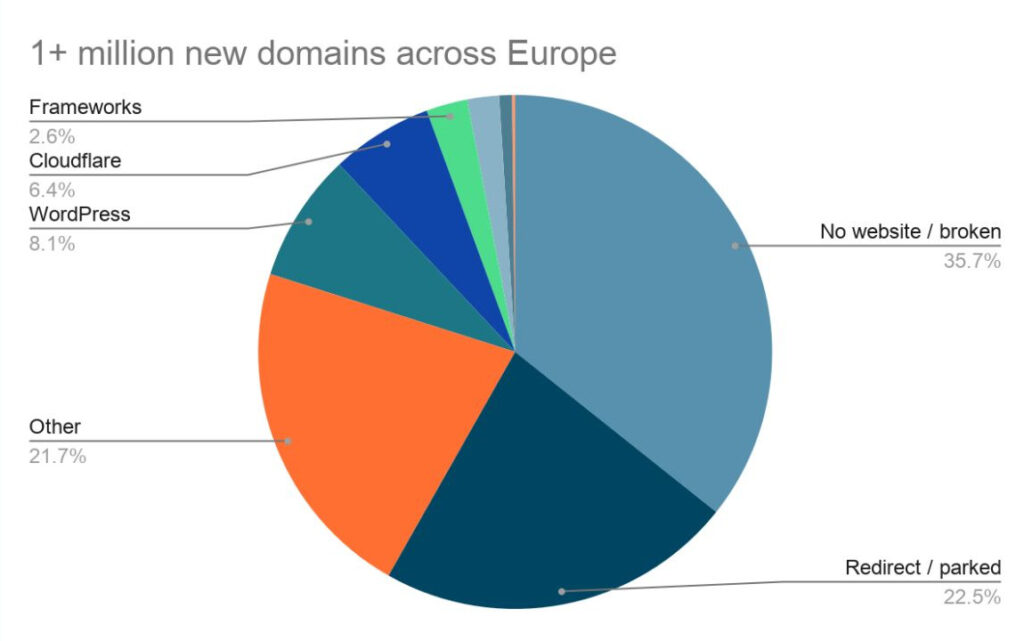

The ShareShift data shows frameworks account for 2.6% of new European domains in the analyzed cohort. That share is small in absolute terms. What makes it significant is the profile of the customer. Vercel alone operates over 233,000 domains across core European ccTLDs, and ShareShift estimates that up to 85% of Vercel’s European intake are new registrations: not migrations from other hosts, but brand-new web projects that never touched shared hosting at all.

Independent financial data corroborates the trajectory. Vercel disclosed a $340 million annual revenue run rate in March 2026, up 84% year-over-year, with coding agents now driving more than 30% of weekly deployments. The developers building those agent-powered projects are not comparing cPanel plans. They are not comparing anything in the traditional hosting market.

WordPress Accounts for 8% of New European Sites. Its Installed Base Is Still 38%.

Perhaps the most significant data point in the ShareShift report concerns WordPress. According to ShareShift’s installed-base analysis, the platform powers roughly 38% of all active websites across European ccTLDs, a figure accumulated over two decades. But in the fresh cohort of domains registered between February and April 2026, WordPress accounts for only 8.1% of new sites.

Distribution of technology across 1+ million new European domains registered in Q2 2026. Source: ShareShift.io

That gap between installed base and new intake reflects a generational shift in CMS adoption. The drop is consistent with broader market data: W3Techs tracking shows WordPress’s overall web share fell from 43.2% to 41.9% between December 2025 and May 2026, marking six consecutive months of decline. The category absorbing displaced share is not a rival CMS; it is sites with no detectable CMS at all, built on modern frameworks or generated directly by AI tooling.

The open question is whether WordPress 7.0, with its native AI client, Connectors screen, and Abilities API for plugin interoperability, can reverse the intake trend. The platform still commands the largest active install base in Europe by a wide margin, and its ecosystem depth has no equivalent among challenger platforms.

Wix at 100%, OVHcloud at 0.66%: The Gap Reflects Business Model, Not Technology Lag

ShareShift’s provider-level data is the sharpest illustration of where the European market stands. The table below shows active site counts and embedded AI adoption rates across five major providers serving European customers.

| Provider | Active Sites (k) | Embedded AI Penetration |

|---|---|---|

| Wix | 7.72 | 100.00% |

| GoDaddy | 12.86 | 26.55% |

| One.com | 5.78 | 17.92% |

| IONOS | 22.98 | 3.42% |

| OVHcloud | 57.06 | 0.66% |

Source: ShareShift.io Q2 2026 Intelligence Report

Wix’s 100% rate is a product architecture outcome, not a coincidence. As a closed platform, Wix controls every site it deploys and has embedded its AI features directly into the onboarding layer: every new site ships with them active by default. GoDaddy’s 26.55% reflects a similar strategy through its Airo product, which auto-generates AI-assisted site content for new customers at signup. One.com’s near-18% rate likely reflects bundling of its proprietary website builder across its European customer base, a regional provider breaking out of the legacy pack through product integration rather than size.

At the other end, OVHcloud operates 57,000 active sites in the cohort, the largest volume of any provider in the dataset, at 0.66% AI penetration. IONOS sits at 3.42% across nearly 23,000 sites. Both are pure infrastructure providers with no owned application layer. Their customers configure their own tools; the host does not control what gets installed or activated. The gap between 100% and 0.66% is not a technology gap. It is a business model gap.

36% of New European Domains Have No Site. AI Builders Are Not Creating Net New Demand.

The ShareShift data challenges one of the more optimistic narratives about AI-assisted site creation. If AI dramatically lowers the barrier to launching a website, the expected result is a wave of new, active sites from users who previously could not build one. The data does not show that.

Across the analyzed European cohort, 35.7% of newly registered domains have no developed website, with no parked page or placeholder content. A further 22.5% redirect or park. More than half of new domain registrations, in other words, produce no active web presence. The ShareShift data is consistent with a picture in which AI site builders accelerate time-to-launch for users who were already going to build something, rather than converting users who would not otherwise have built at all — though the data does not include historical dormant-rate comparisons that would confirm this directly. The dormant share of new registrations represents near-term churn risk for any host that counts domains rather than active sites as its primary metric.

14% of New Sites Already Have llms.txt. Defaults Are the Strategy.

A secondary finding in the ShareShift report concerns Answer Engine Optimization. As AI assistants and search tools like ChatGPT, Perplexity, and Google AI Mode increasingly serve as discovery surfaces for small businesses, some providers are beginning to prepare customer sites for that traffic by default. ShareShift found that 14% of all new sites in the cohort now include llms.txt files or equivalent AEO signals. A further signal: Cloudflare’s content-signal header is active on 25% of all Cloudflare-operated sites in the dataset.

Both figures underscore the same point visible in the AI adoption table: at internet scale, defaults are the strategy. Platforms with direct control over the application layer, such as Wix, GoDaddy Airo, and Cloudflare, can deploy new capabilities across their entire installed base without any action from the end customer. Infrastructure providers that hand raw compute to customers cannot.

Methodology note: Data in this article comes from ShareShift.io’s Q2 2026 Intelligence Report, based on analysis of over three million new active domains across European ccTLDs and the .ai zone. ShareShift is a commercial market intelligence provider. “Embedded AI Penetration” measures the share of active sites with AI-powered features detectable at the application layer; the firm’s full methodology is available in the underlying report. WordPress installed-base figures are from W3Techs (May 2026). Vercel ARR and growth data from TechCrunch (April 2026).